Subject-to is one of those strategies that sounds complicated until someone explains it in plain English. Then it sounds almost too simple.

The short version: you buy a property and take over the seller's existing mortgage payments without formally assuming the loan. The seller's name stays on the mortgage. You take the deed. You make the payments. The bank doesn't necessarily know ownership changed.

That setup has real advantages in a high-rate environment, and real risks that every investor needs to understand before structuring one of these deals. Here's how it actually works.

The plain-language mechanics

In a standard purchase, you get a new mortgage, the seller's old mortgage gets paid off at closing, and you start fresh. In a subject-to deal, none of that happens. The seller's original mortgage stays exactly as it is, same lender, same interest rate, same loan terms, same seller's name on the loan, and you take the deed.

"Subject to" means you're buying the property subject to the existing financing. You don't pay it off. You don't assume it through the lender. You simply take ownership and start making the payments the seller was making.

A concrete example: a seller bought a house in 2021 at a 3.25% interest rate. They're now in financial distress and need to sell fast. They've paid off very little of their mortgage or the value of the house may have gone down, so if they sell now with a realtor, after realtor commission and closing costs, they would lose money. Current mortgage rates are 6%. If you can take over that 3.25% loan through a subject-to deal, you've acquired the property at a dramatically lower cost of capital than any new financing would allow. The seller gets out from under the payments and the property. You get the property with a below-market interest rate baked in.

Why it's gained momentum in 2026

Subject-to deal volume is at levels not seen since the onset of the Great Recession. The combination of a large pool of low-rate assumable mortgages and a growing population of distressed sellers attached to those mortgages is not a coincidence, it is a market condition.

Millions of homeowners locked in 3-4% mortgages between 2020 and 2022. Many of those same homeowners are now experiencing the financial distress that motivated sellers always experience, divorce, job loss, pre-foreclosure, inherited property they don't want, but they're sitting on mortgages that would be impossible to recreate at today's rates.

For investors, taking over a 3.25% loan on a property that would otherwise require new financing at 7%+ isn't just convenient. On a $200,000 loan, that rate difference is roughly $650/month in lower payments. That's the difference between a deal that cash flows and one that doesn't.

Who it works for as a seller

The seller in a subject-to deal is almost always someone in financial distress who needs out of the property faster than a conventional sale would allow, or who has no equity to work with.

Pre-foreclosure sellers facing auction are the classic use case. They can't sell conventionally in time, the bank is at the door, and having someone take over the payments stops the foreclosure clock immediately. They walk away with their credit damage minimized instead of a foreclosure on record.

Sellers who are underwater, where the mortgage balance minus selling costs exceeds the property value, can use a subject-to deal to exit without bringing cash to closing to cover the gap. In a conventional sale they'd have to pay the difference. A subject-to buyer takes the mortgage as-is.

Divorce situations, inherited properties, landlords who've stopped managing and just want out, any seller whose primary goal is speed and exit over maximizing price is a potential subject-to candidate.

What the buyer gets and what they're taking on

What you get:

- Below-market interest rate on an existing loan

- No mortgage application, no underwriting, no lender fees

- No or minimal down payment (typically you pay the seller the difference between the mortgage balance and your agreed purchase price in cash)

- Fast closing, no lender timeline to wait on

What you're taking on:

- Full responsibility for payments even though the loan isn't in your name

- The seller's credit is affected if you miss payments, their name is still on the mortgage

- The property itself as collateral, if you stop paying, foreclosure runs against the seller's credit, not just yours

- The due-on-sale clause risk (covered in detail below)

The cash you bring to closing is typically the equity the seller has in the property. If the seller owes $150,000 on a property worth $200,000, you might pay them $20,000-30,000 at closing to make the deal work for them, while taking over $150,000 in mortgage payments. You get immediate equity.

The due-on-sale clause is the real risk you need to understand

Most mortgages contain a due-on-sale clause, a provision that gives the lender the right to demand immediate full repayment of the loan if the property is transferred without their consent. In a subject-to deal, the property transfers. The lender technically has the right to call the loan.

This is not a hypothetical risk. It's a contractual right the lender holds. Subject-to transactions are technically legal, but they operate in a gray area. The buyer takes title and responsibility for the home, but the seller remains on the mortgage.

The practical risk in 2026: historically, enforcement was uncommon when interest rates were declining. With rates rising since 2021, lenders have greater incentive to call low-rate loans to replace them with higher-rate ones. If the clause is enforced, the buyer must pay off the loan immediately or risk losing the property, leaving the seller liable for any shortfall.

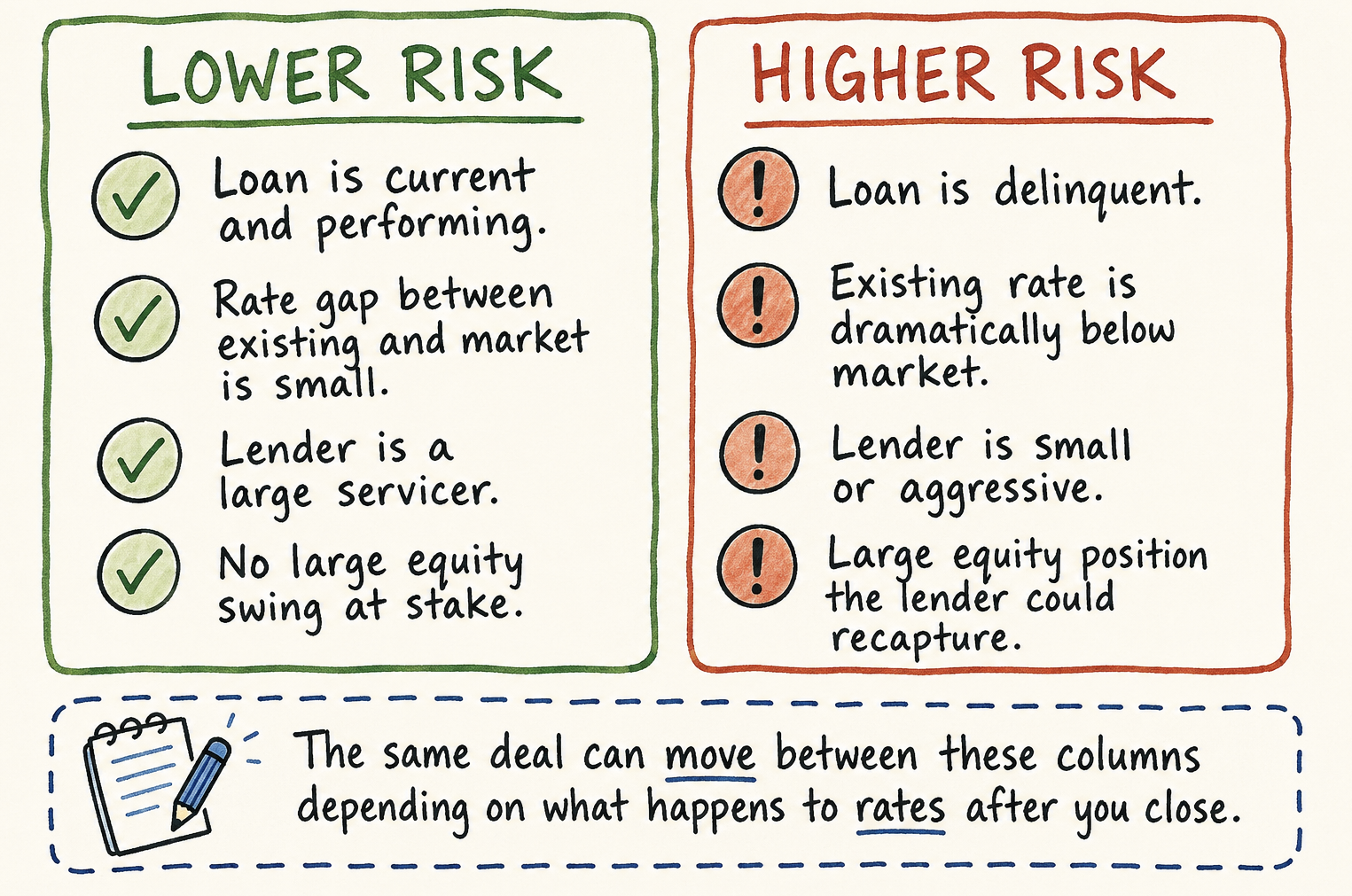

The counterpoint: so long as the interest rate on the existing loan is within a few percent of market rates and the loan is performing, the lender is not likely to accelerate it. It costs money in legal fees to foreclose a mortgage, and the lender would rather get paid than have another non-performing loan on its books.

The honest truth: the due-on-sale risk is real, not theoretical. It's lower when the loan is performing and the rate gap isn't enormous. It's higher when the lender has a clear financial incentive to call the loan and reinvest at market rates.

Investors still do these deals because the math works even with the risk priced in. A 3.25% loan in a 7% rate environment isn't just cheaper financing, it's financing that often can't be replicated at all. That spread is the entire reason subject-to exists as a strategy. Most servicers don't audit ownership changes on performing loans, and a loan that's getting paid on time rarely draws attention. Going in, you need a plan if the loan does get called, enough cash reserves to refinance quickly, or an exit timeline that doesn't depend on holding indefinitely.

Key protections and structuring considerations

Keep the loan performing. This is the most important protection. A lender whose loan is current and generating payment has little incentive to trigger expensive foreclosure proceedings. Miss a payment and everything changes.

Use a land trust. Placing the property in a land trust with the seller as the initial beneficiary, then transferring beneficial interest to the buyer, doesn't hide the transfer from public record; deed transfers are always recorded. What it does is remove your name as the named grantee. The deed shows the trust, not you. Servicers monitoring for ownership changes are looking for individual name transfers. A land trust reduces that signal without eliminating the underlying legal reality.

Protect the seller in writing. The seller's name stays on the mortgage. If you stop paying, their credit takes the hit and they face foreclosure. A properly drafted subject-to agreement must include provisions that protect the seller — a power of attorney, notification requirements, and clear remedies if the investor fails to perform. Sellers need to understand what they're agreeing to, and investors who don't protect their sellers damage their reputation and face legal exposure.

Work with an experienced real estate attorney. Subject-to deals have more legal complexity than a standard wholesale assignment. Have your attorney review the specific loan documents, draft the subject-to agreement, and advise on the due-on-sale exposure for your state and loan type before you close your first deal.

What makes a good subject-to deal

The interest rate gap is the primary driver of value. Taking over a 3.25% loan when new financing costs 7% is a powerful advantage. Taking over a 6.5% loan when new financing costs 7.25% saves much less and doesn't justify the additional complexity and risk.

The property needs to cash flow at the existing payment. Run the full rental analysis, NOI, debt service coverage, monthly cash flow, using the existing mortgage payment. ChatARV's buy-and-hold calculator runs this analysis from actual comp data, so you know whether the deal works at the seller's rate before you negotiate the terms. Run your numbers here.

The seller's equity position matters. Deep negative equity deals require careful structuring and specific exit strategies. Deals with meaningful equity give you more options if circumstances change.

The seller needs to genuinely understand what they're agreeing to. A seller who later claims they didn't understand the loan was staying in their name creates legal and reputational exposure. Full disclosure, in writing, with time for the seller to consult their own attorney, is not optional.

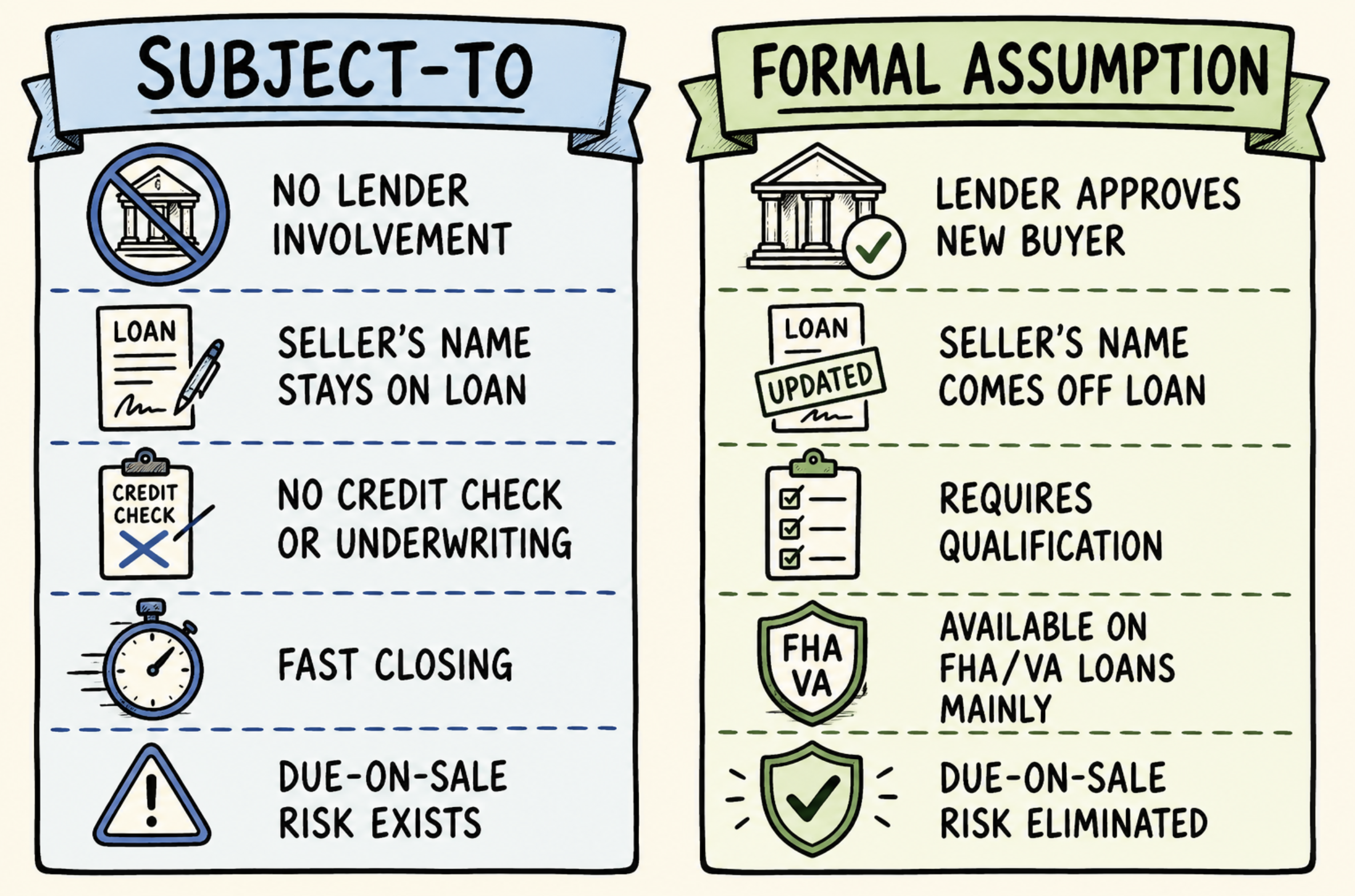

Subject-to vs loan assumption, the difference

These are often confused. In a formal loan assumption, you apply to take over the existing mortgage through the lender, they underwrite you, approve you, and transfer the loan into your name. The seller's name comes off the mortgage completely.

In a subject-to deal, there's no lender involvement at all. Their name stays on the loan. You never contact the lender. The deal is structured between buyer and seller only.

Formal assumption eliminates due-on-sale risk but requires lender qualification and is only available on certain loan types (FHA and VA loans are assumable by design; conventional loans usually aren't). Subject-to is a tool to use if you're working with a conventional non-assumable loan, but carries the due-on-sale risk exposure as a tradeoff.