Novation agreements

Most wholesalers learn the assignment of contract first and use it on almost every deal. Novation stays in the background until the moment an assignment won't work. When that happens, it becomes the only tool that keeps the deal alive.

Understanding what novation actually is, how it differs from assignment, and when it makes sense will add a meaningful exit strategy to your toolkit. It won't replace assignment. It solves problems assignment can't.

What novation is

The core idea: a novation agreement lets you fix and flip a property without ever buying it. You promise the seller a number, renovate the property, sell it to a retail buyer, pay the seller what you promised, and keep everything above that. The seller gets more than the cash offer on the table. You avoid closing costs, hard money fees, title insurance, and lender timelines.

More specifically: you put a property under contract with a seller at a price that works for you, then list it on the MLS and find a retail buyer yourself. When a buyer makes an offer, the seller signs a new contract directly with that buyer. Your original contract gets cancelled. The seller walks away with their net proceeds, the end buyer gets the property, and you collect the spread between your contract price and what the end buyer paid, structured through the title company at closing.

You're not assigning your contract. You're replacing it. The seller has to agree to this upfront, in writing, before you list anything.

The catch is that if the property doesn't sell at your target price, you go back to the seller and renegotiate down. Novation deals usually need to be priced a bit below retail to move. Your profit lives in the gap between what you locked it up for and what the market pays.

How it's different from assignment

This is where most people get confused, and the confusion matters.

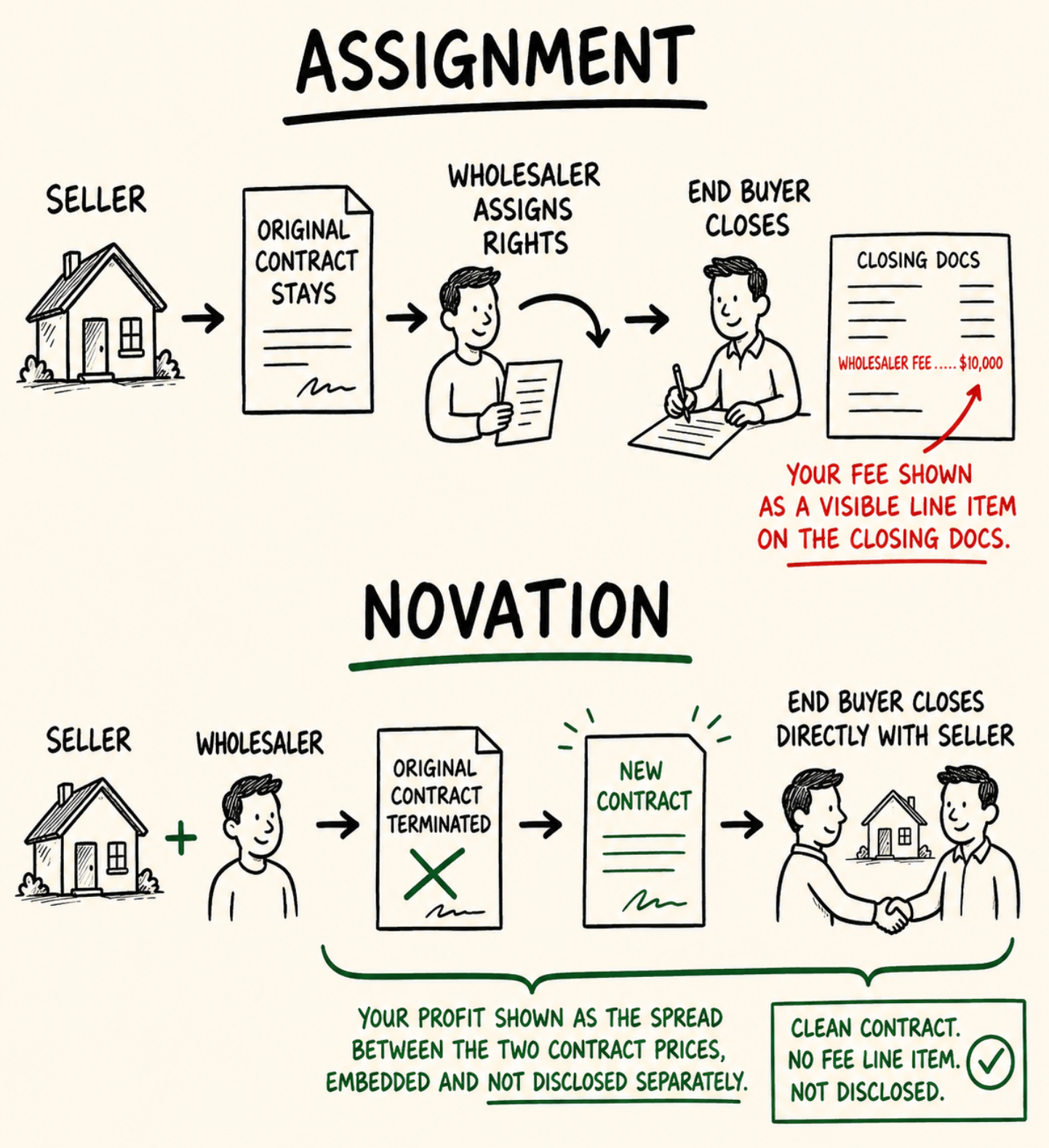

In an assignment, your original purchase contract with the seller stays in place. You transfer your rights under that contract to an end buyer. The contract itself doesn't change, only who holds the buyer's position. Your assignment fee appears on the closing statement as a line item. The seller can see it. The buyer can see it. The title company sees it.

In a novation, the original contract is terminated. A new contract is created directly between the seller and the end buyer. You're removed from the transaction entirely. Your profit is embedded in the price difference between what you contracted to pay and what the end buyer pays, and doesn't appear as a disclosed fee anywhere. The end buyer and lender see a clean purchase contract with no wholesale activity in the chain.

The legal difference is significant: unlike assignment, novation completely releases the original party from liability. Once the novation is signed and the new contract is in place, you have no remaining obligations to the seller and no exposure if the deal falls apart after that point.

The three ways to structure a novation

There isn't one version of a novation agreement. There are three, and which one you use depends on whether you're licensed, how you're funding the renovation, and how aligned you and the seller are on price.

1. Net listing

A licensed agent goes to the seller and guarantees a number in writing, say $300,000 on a property worth $400,000 ARV. The agent cleans up the property, lists it on the MLS, finds a retail buyer at full ARV, receives the proceeds at closing, pays the seller the guaranteed amount, and keeps the difference minus costs. The seller gets their number. The agent keeps the spread.

2. Standard novation

The same structure without a license. As a real estate investor, you sign a novation purchase agreement guaranteeing the seller $300,000. You fund the renovation yourself or with a private lender, find a retail buyer, sell at $400,000, pay back your renovation financing, pay the seller their $300,000, and keep what's left. No hard money loan, no title insurance, no closing costs on an acquisition. You never bought it.

3. Partnership with the seller

This structure works when the seller believes the property will sell for more than you're projecting. Instead of fighting over a number, you split the upside. A common arrangement: anything up to the seller's minimum is theirs, everything between that floor and your projected ARV is yours, and anything above your projection is split. The seller who's convinced their house will sell for $425,000 now has skin in the game to let you prove it.

Why it matters in practice

Three situations make novation the right tool instead of assignment:

1. Your buyer is using financing

FHA, VA, and conventional loans run through lenders who underwrite the purchase contract. If that contract has an assignment clause or shows wholesaling activity, underwriters often flag it or decline to fund. But if the buyer is substituted via novation, the loan underwriter sees a clean contract with no wholesale activity, exactly what they want to see.

This is one of the most important practical applications. Assignment of contract narrows your buyer pool to cash buyers and hard money borrowers. Novation opens it to the entire retail financing market. More buyers means more competition for your property, which means higher prices.

2. You want to list the property on the MLS

You cannot list a property on the MLS under an assignment of contract. You don't own it, and you have no authority to market it as property. You can only market your equitable interest, the contract itself, to other investors.

Under a novation, you have the seller's consent to market the property on the open market. This allows you to price the property at or near retail value, run a standard listing, receive competing offers from retail buyers, and negotiate a much higher net profit than a typical assignment fee would produce.

A standard wholesale assignment fee on a move-in ready home might net $8,000-12,000. A novated deal on the same property, listed on the MLS at retail pricing, can produce $20,000-40,000 or more.

3. Your assignment fee is too large to disclose

If you're wholesaling a deal with a $50,000 spread, showing that number on the closing docs via assignment can kill the deal. Sellers may feel taken advantage of when they see the number. Buyers may question whether they're overpaying. A large visible fee creates friction that often unravels the transaction.

Novation buries the spread in the price difference between contracts. There's no line item. The seller sees their net proceeds. The buyer sees their purchase price. The spread is simply the difference between those two contracts, paid at closing.

How a novation deal actually works

The mechanics differ from assignment in a few important ways.

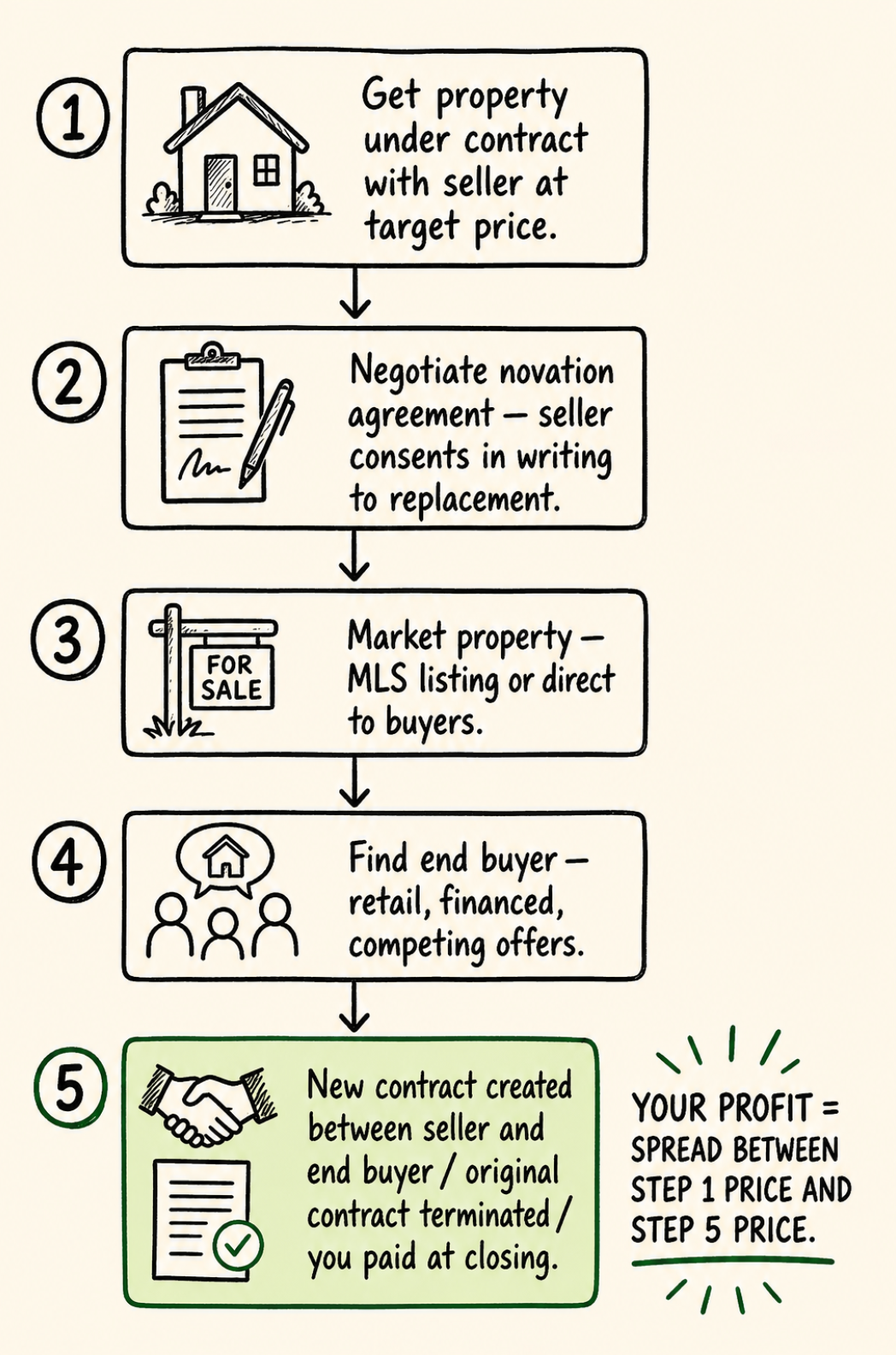

You get the property under contract with the seller as you normally would, a purchase agreement at a price the seller accepts.

You then negotiate a novation agreement with the seller. This document requires the seller's written consent to terminate the original contract and replace it with a new one involving a new buyer. Transparency is non-negotiable. If the seller isn't 100% clear on what's happening, don't do the deal. The seller needs to understand they're agreeing to sell to someone else at a potentially higher price, and that you're profiting from the difference.

You market the property, either directly to buyers or via an MLS listing if you have the right structure in place, and find an end buyer.

When the end buyer is found, a new purchase contract is created between the seller and the end buyer. The original contract is terminated. Your novation agreement governs how you get paid at closing, typically as a consulting fee, transaction coordination fee, or as the difference between the two contracts facilitated through escrow.

The title company handles the mechanics at closing. Using a wholesale-friendly or novation-experienced title company is important. Not all title companies are set up to handle this structure. Find one in your market before you need one.

Timeline: novation deals take longer than standard assignments. The seller signs the final closing documents and receives their payment, typically within 1-2 months from the start of the process. If your seller needs to close in two weeks, novation is the wrong tool.

The real risks

Licensing gray areas. This is the most important issue and it varies significantly by state. Marketing a property you don't own to retail buyers can look a lot like acting as a real estate agent. In states with strict licensing requirements, novation can put unlicensed investors in a legally exposed position. Consult a real estate attorney in your state before your first novation deal. The conversation costs $200-400 and protects you from a licensing complaint.

All three parties must genuinely consent. Novation isn't valid unless the seller understands and agrees in writing to what's happening. A seller who felt pressured into signing, or who didn't understand they were agreeing to a new buyer being substituted, has grounds to void the transaction. Disclose clearly. Get signatures on everything.

Longer timelines mean more exposure. While your assignment deal might close in two to three weeks, a novation with an MLS listing and retail buyer financing can take 45-60 days. During that time you're holding an original contract with the seller. If market conditions shift, the seller gets cold feet, or something surfaces in inspection that changes the deal, you have more exposure than a fast assignment close.

Not every title company can do it. Find your title company before you find your deal. A title company that's never processed a novation will slow everything down or decline to close.

When novation makes sense vs when it doesn't

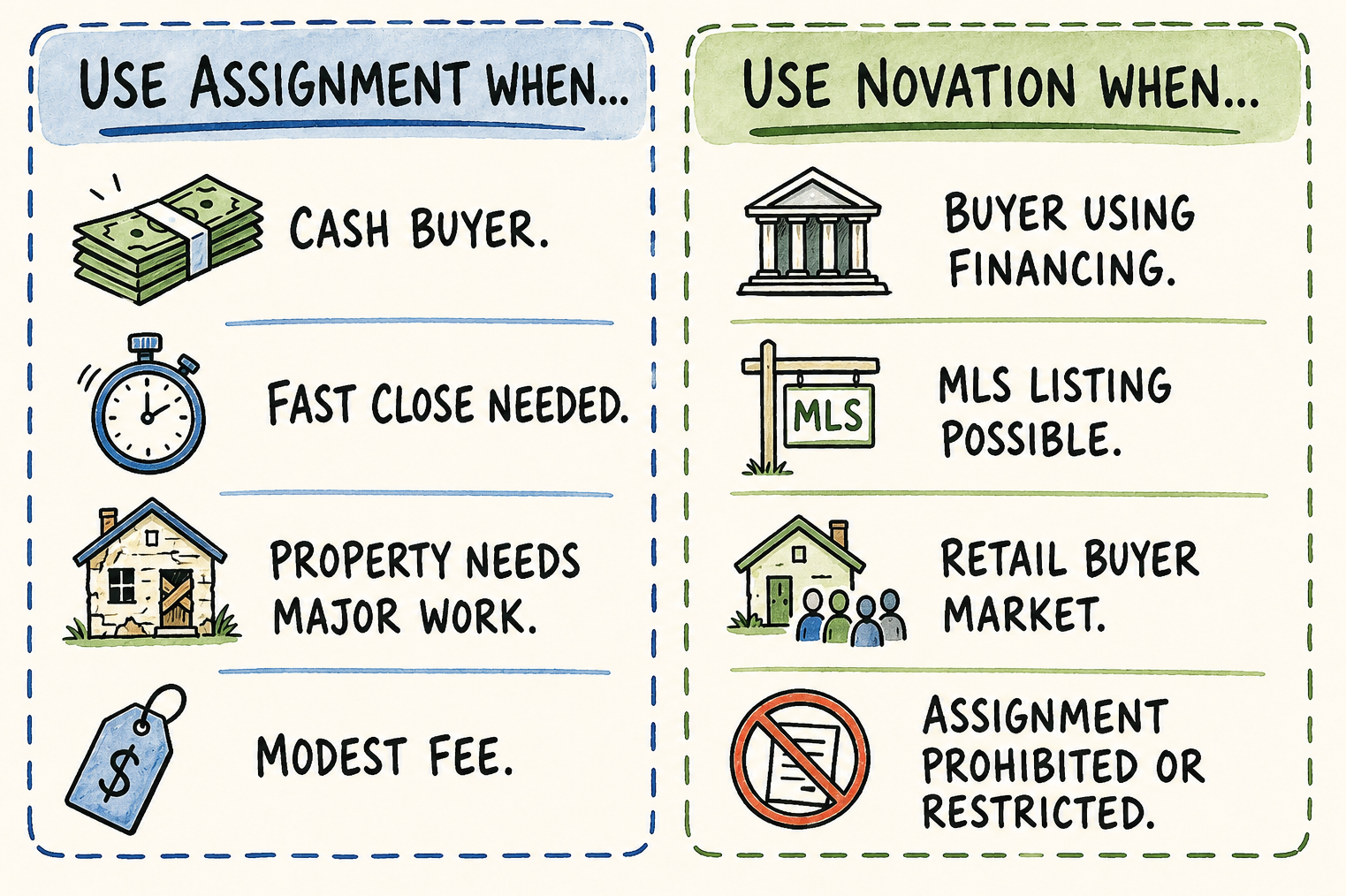

Use novation when:

- Your best buyer is using FHA, VA, or conventional financing

- The property is in good enough condition to list on the MLS and attract retail buyers

- You want access to the full retail buyer market, not just cash investors

- Standard assignment is prohibited by the original contract or local law

Use assignment when:

- Your buyer is a cash investor who closes fast

- You need to close in under three weeks

- The property needs significant work and retail buyers aren't realistic

- The fee is modest and visibility isn't a concern

- You want simplicity and speed

Assignment contracts still work. They're faster, simpler, and more common. Novation isn't better than assignment. It solves problems assignment can't. A financed buyer, a retail-ready property, a market where assignment is restricted: those are the situations where novation earns its place

Run your numbers first

ChatARV's As-Is mode includes a novation deal structure alongside wholesale, creative finance, and buy-and-hold options. It calculates your ARV from actual comps, estimates repair costs, and runs the novation math: contract price, estimated retail sale price, and net profit before you commit to the structure. Run your numbers here.